This great blog post from Nick Maguilli illustrated the peris of retiring when the market is entering a prolong downtrend:

https://ofdollarsanddata.com/great-depression-or-bust/Without any context, people may assume that retiring when the market is falling is a good thing for what it means for your SWR because:

- you didn't retire right at the peak - hurrah!

- valuations are slightly lower - all in all this should slightly elevate future returns

However the more pressing factors are is that you are retiring in a term downtrend and what this may imply for the more immediate future. Under such conditions:

- stocks do considerably worse over the short term than on the whole (5.5 vs 9.6%)

- You are at immediate risk of the small downtrend now extending into a much larger and longer downtrend

- volatility increases and you should expect a bumpier ride

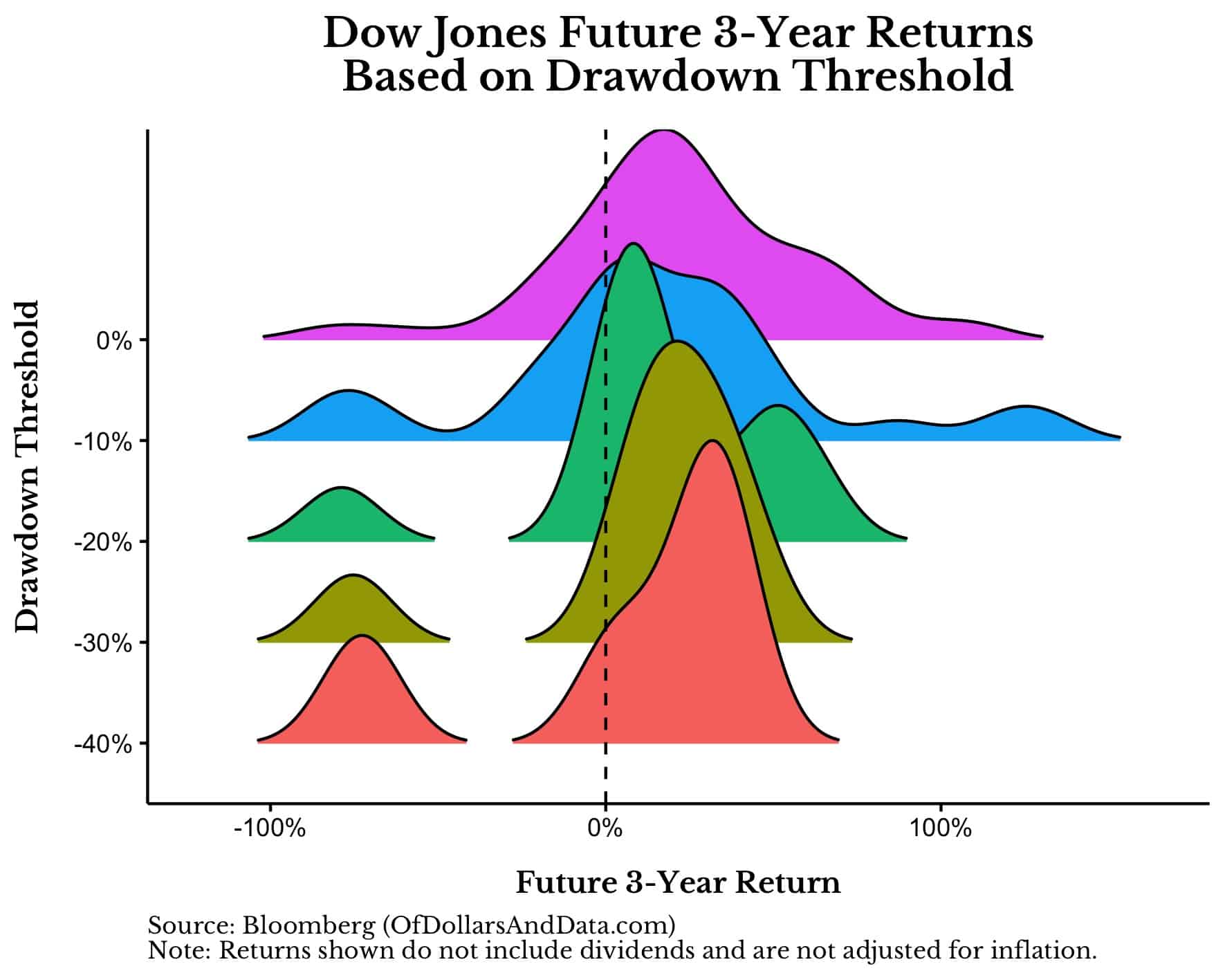

Over 3 years, while the expected return improves, the distribution of those returns is all over the place, argely due to the depression dominating this still relatively small subset of the overall data:

Up to -20% drawdowns the average/median 12 month outlook is still lower than. It's only after the market has really crashed (-30% or worse) that you can be relatively confident that the bottom is already or close to being in, and the 1yr outlook improves - we are not at that stage yet.

And even if and when it does fall that much and the immediate outlook is higher, remember that crucially, retirement planning is based around planning for the worst case scenario to gaurantee not running out of money. While the outlook may be good, the risk of a cataclysmic outcome must still not be written off.

All things said, and to point out the somewhat bleedin' obvious, it is much better to retire during a bull market, preferably one that has many years left to run!