You can also skip asset reporting on FAFSA under the new rules if a family member has been on Medicaid in the previous two years. See the FAFSA simplification law section 479(b)(2)(D).

I am planning to see how much money I need to put into the 529 accounts for my kids. We are a low spending family. So we can get onto medicaid when we FIRE.

Medicaid is based on income, not spending, so you'd need to be a low income family for at least a few months to get on Medicaid. But you're right in that being a low spending family makes it easier to be a low income family. The potential problem, which may or may not affect you, is "forced income", such as if you had a big pension or large investment income.

Is this article what you are referring to?: https://www.csac.ca.gov/sites/main/files/file-attachments/summary_of_changes_for_the_2024-25_fafasa.pdf

I was referring to the actual law, but the document you linked to does seem to be a pretty good summary of the law and contains a reference to the same thing when it says

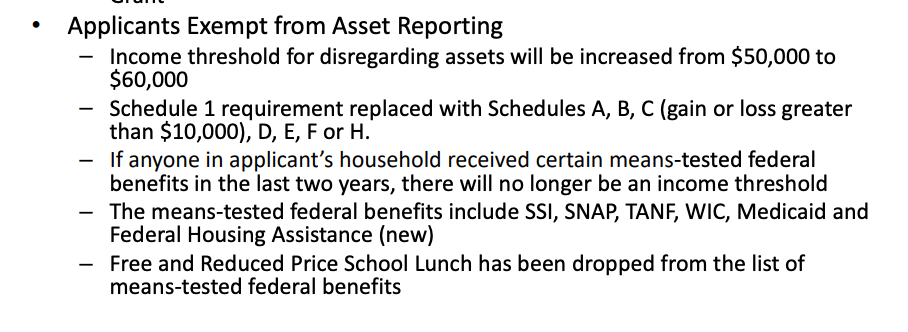

"- If anyone in applicants household received certain means-tested federal benefits in the last two years, there will no longer be an income threshold

The means-tested federal benefits include SSI, SNAP, TANF, WIC, Medicaid and

Federal Housing Assistance (new)"

Also, according to these rules:

If income is less than $60K, there will not be asset test either.

I think the $60K income requirement also requires you to not file a slew of IRS schedules, including, of interest to you, Schedules B and D. But if you're on Medicaid (see above), that would be sufficient to avoid the asset test anyway.

With these info. If I can get onto medicaid two years before my first kid goes to college, I can get financial aid even I have a big investment account, right? Does this mean I won't need to put money into their 529 accounts if I can plan this out correctly?

Regarding your first question, it's anyone in the family any time in the prior two years (I think - doublecheck that), so getting on Medicaid in the calendar year spanning spring of sophomore / fall of junior year would be sufficient.

And it would exempt you from asset reporting, so a big investment account wouldn't count against you *for FAFSA purposes*. Some schools use other financial aid methods in addition to FAFSA, and the rules for that are different.

Regarding your last question, if you're really opposed to 529s for some reason, sure, your approach can work. But even ignoring FAFSA, 529s are quite good for college savings, and even more so if you get a state tax benefit. With the state tax benefit, you get tax-deferred compounding, tax-free withdrawals, the ability to keep the money out of your estate, the ability to roll the 529 to other relatives, and the ability to roll excess into the kid's Roth IRAs (with certain constraints).

I would probably stay away from 529s only if funding them would require me to realize really high capital gains (like if I had already saved a bunch in taxable), if there were significant doubt if my kids would go to college and I didn't like the modest penalties for non-college withdrawals, if I only had one kid, or if I didn't have any nieces/nephews/grandkids that I wanted to help out.