This seems like an appropriate place for this article.

http://www.economist.com/news/finance-and-economics/21677245-growth-firms-selling-computer-generated-financial-advice-slowing-does-not

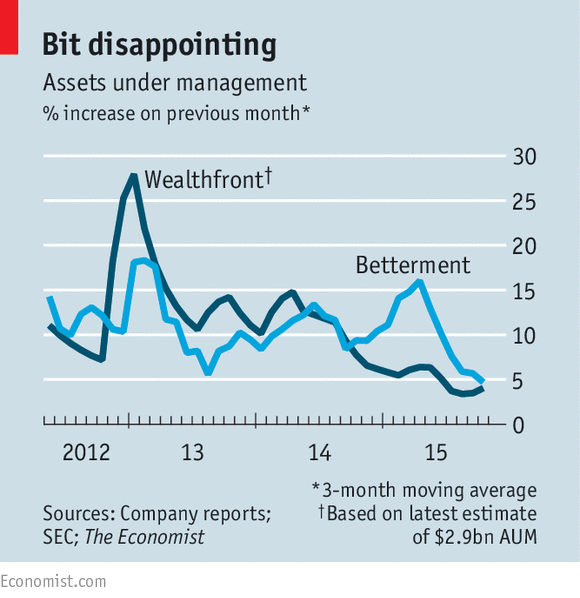

Robo-advisors see slower growth, and probably have trouble being profitable.

In my opinion this is the biggest risk with giving one of these tech startups your money. If they go under, or if their VC investors decide they aren't making enough money and they increase their fees, you're left with one of two choices:

1. Sell everything and pay a steep capital gains taxes.

2. Move the entire 10-20 fund portfolio they put your money in, over to another broker like Vanguard, and be stuck manually managing those 10-20 funds for the rest of your life.

Considering these robo-advisors were made to be a simple choice, making things easy for the financially-illiterate...and considering the failure rate for tech startups, it just doesn't seem like a wise move. Especially when Vanguard's version has all the same simplicity, for half the cost.

At first that chart confused the hell out of me. How did they have the most assets under management back in 2012? And haven't they been advertising a ton, why are their assets under management shrinking.

Then I saw the graph was PERCENT INCREASE over previous month, not absolute assets.

Jesus. That chart shows the opposite of what it says. They're growing, monthly, by ridiculous amounts.

Yes, the growth is slowing, but that's because it's a percentage, and as their asset base gets larger, it's harder to grow a larger percentage.

I'm no fan of those companies, but that chart is pretty good for them.

Let me know when they're negative percent (I.e. People are taking more out than putting in) for two months in a row (or even once).

If they're growing 5% a month right now, that's still a RIDICULOUS rate of growth.