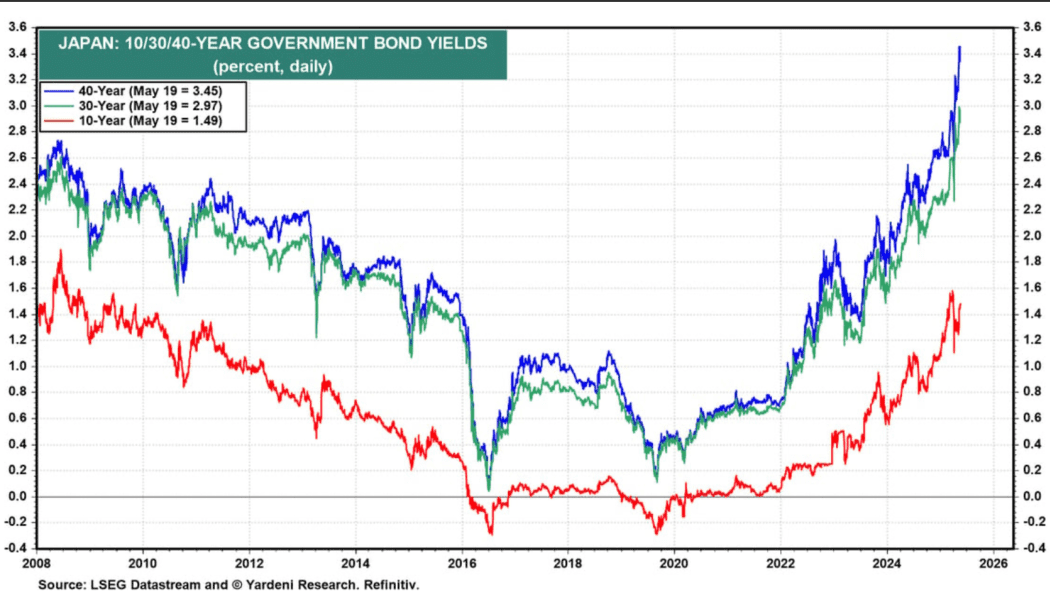

Japanese bond yields have soared, as "bond vigilantes" have gone on strike. Japanese 30y bonds have gained about a full one percent of yield since the start of this year. Their 40 year bonds have gone up about 1.5%. I can't help but to think this looks a lot like what happened in the US in 2022-2023, which eventually culminated in a small banking crisis and deposit flight. Bond convexity when coming off of very low yields is extreme.

Article:

https://www.marketwatch.com/story/bond-vigilantes-are-sending-warnings-globally-what-does-that-mean-for-your-portfolio-545944c3?mod=home_leadIt's fair to ask where the investment flows are going.

European stocks (Germany, France, Spain, Italy) are having a moment in the spotlight, as Euro rates are cut, but these don't seem to be alternatives to Japanese bonds. In

the bond world, yields of Brazil, Mexico, India, and South Korea have fallen YTD, so they are suspects. Their debt-GDP ratios are 87%, 50%, 82%, and 52%, respectively, compared to 255% for Japan. One also has to wonder if yields in the US (debt/GDP=122%) would be much higher if not for reduced demand for Japanese bonds and the expectation of rate cuts later this year that could make US treasuries bought today go up in value.

In a world of tariff-siloed economies, maybe heavily-indebted, mercantilist Japan doesn't look as much like a safe haven. Mexico and SK have low debt-to-GDP. Meanwhile, Brazil and India are about to launch BRICSpay to divorce themselves from dependency on USD-denominated international systems and presumably reduce their odds of being squeezed by events in that sphere.

The Japanese carry trade, where yen are borrowed, sold for USD, and invested in treasuries at higher interest rates than the loans, may have run low on lenders willing to loan at low rates against increasingly-risky US treasuries.

Moods could shift about the probability of US rate cuts if tariffs raise inflation and extend the FOMC's pause on rate cuts.

Imports are about 14% of US GDP, so if those costs go up an average of, say, 10%, then that's roughly a +1.4% increase in spending/costs, not accounting for retail markups on the higher amounts. Plug in your own numbers and do your own calculations, but it seems CPI in the 3rd and 4th quarters will be zooming up above 3% unless there is a complete policy reversal. Recessionary conditions by then

seem unlikely, so will the FOMC vote to cut rates in the face of rising inflation?

While we speculate, Japanese stocks look like maybe they shouldn't be up +7.63% over the past month. An EWJ put or bear spread is interesting at the moment, on the thesis that banking issues might be about to erupt.