I also find Dalios ideas fascinating. They are a cautionary tale about extrapolating the past into the future, which is what we are all doing when we use a particular currency to buy particular financial instruments that exist within a particular legal era, because they did well for a couple of generations in the past. Dalit also gets me thinking about how things change - its because things have to change.

There is however an element of early 20th century classical economics to Dalios assumptions. He explicitly states in some places that as debt levels increase, there comes a point when interest rates increase (as a result of investor reactions to risk and leverage). Rising rates choke economic growth, which makes the debt more burdensome, etc. This is at odds with the expectation of a low interest rate future. Such theories have an element of unfalsifiability, because year after year the theoretical tipping point seems just around the corner. People were talking about imminent hyperinflation in 2010 too. Still waiting.

Agreed about extrapolating the past into the future and denominating in a currency implicitly buying into that narrative. The question is what is the right way to invest moving into the future?

I would like to invest in China, but they are not shareholder friendly to foreign investors. EM and international are being trashed by having to buy US dollars which the treasury is happy to print as long as they can to keep our domestic companies happy and debt manageable. For the near/middle term - I think that means stay invested domestically and take advantage of the USD position as the reserve currency.

I don't like the 20% gold allocation, but it is the only uncorrelated asset i can find that is not a bond. I think tech and biotech benefit from cheap debt and utilities are actually in a good position for the first time in 30 years as the nation's transportation infrastructure electrifies. Right now the utilities own the means of production and buy fossil fuels from the big energy companies. This will lessen as the grid transitions in a green direction. I don't know if you keep up with the advances happening in fusion energy, but there is a chance the utilities will own all the means of production and generation.

Here is the theory behind the portfolio (posted previously on bogleheads):

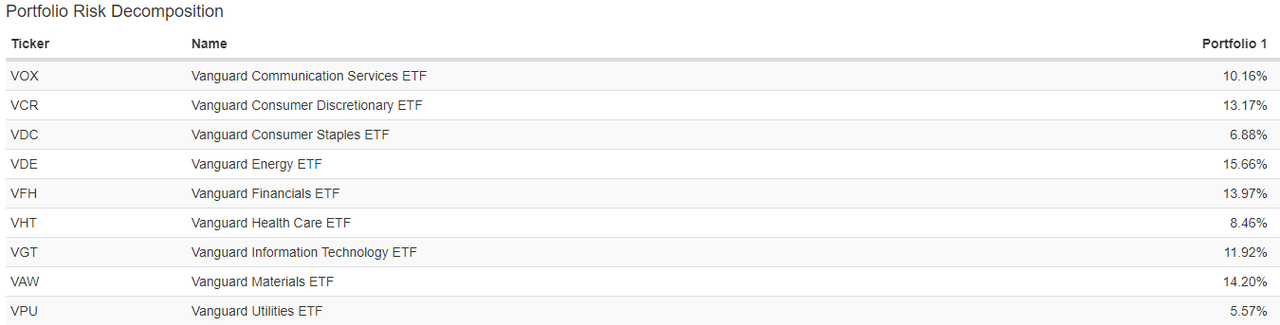

I don't think bonds are an ideal asset class going forward, but the negative correlation to equities makes them ideal for risk parity strategies. Risk parity works because the negative correlation of LT Treasuries blunts the decline of Equities - rebalancing and leverage allows the strategy to outperform. My idea is to use less volatile equities and gold to accomplish the same goal. Gold is not as efficient as LT treasuries as a hedge so the equity portion has to be less volatile. What are the least volatile sectors in the market? Here is an equal weighted sector portfolio with risk decomposition shown:

Utilities, Consumer Staples, and Healthcare

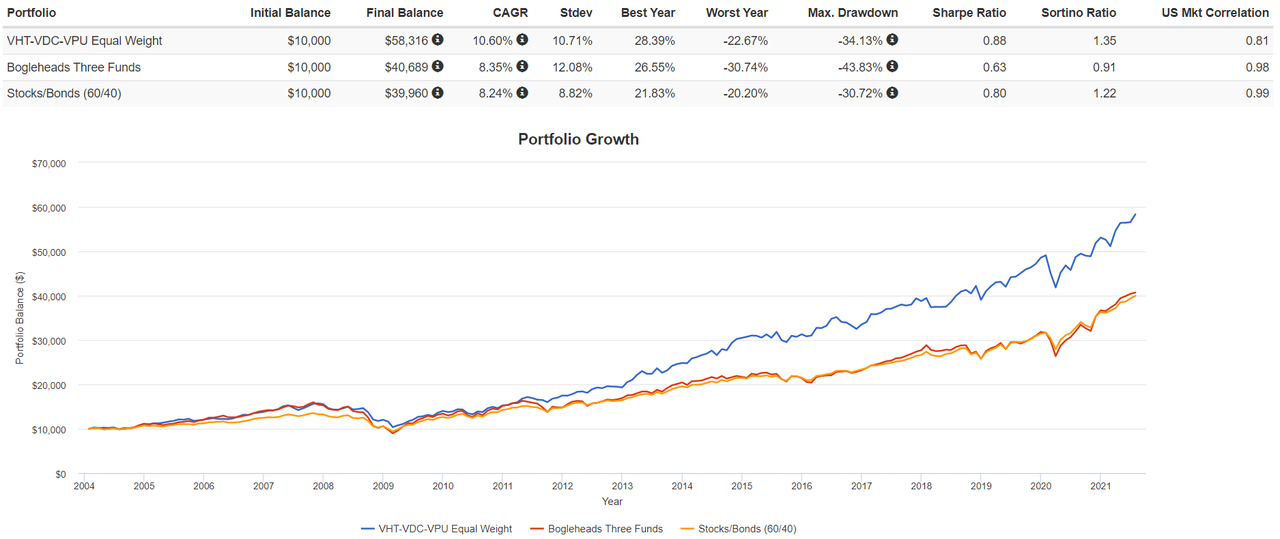

Here is a back test of an equal weight portfolio of these low risk sectors:

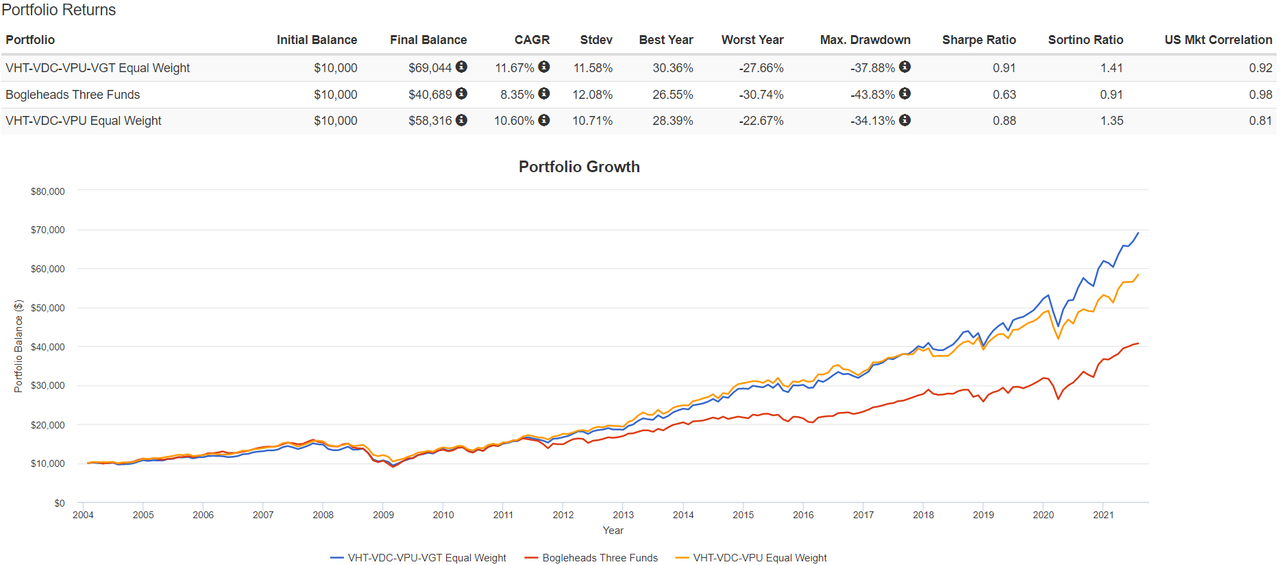

I wanted to incorporate my theme of continued American innovation and include technology. I like that utilities have heavy debt loads (benefit from money expansion) and they should benefit from electrification of vehicles. Here is the same portfolio with technology added in:

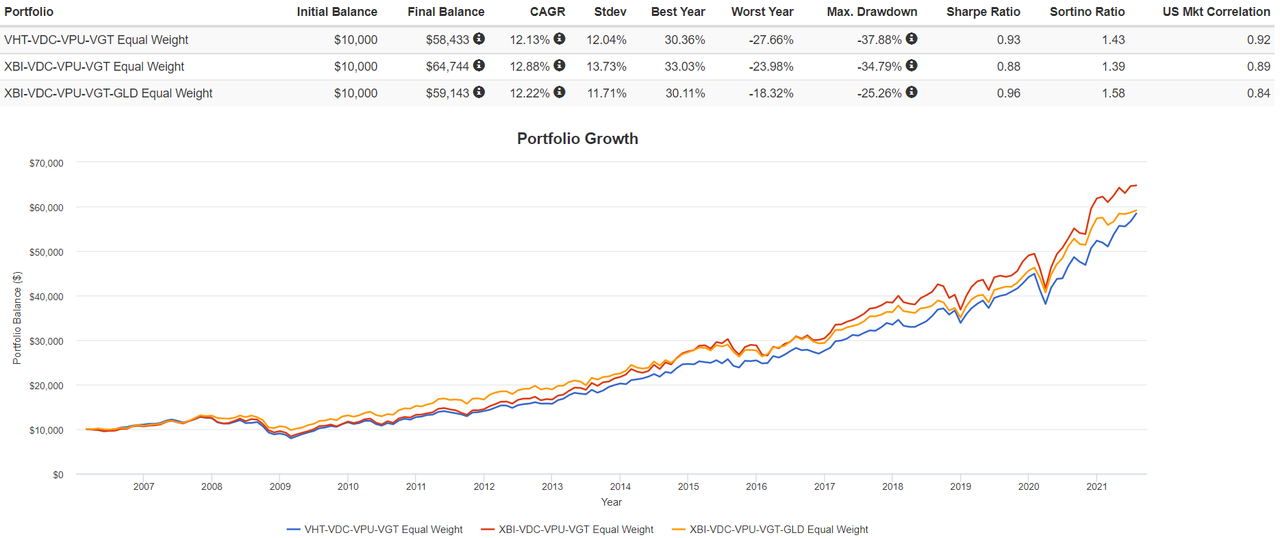

Now continuing with the theme of American innovation - I wanted to add biotech to the portfolio. I really like the ETF XBI - which tracks an equal weighted small cap biotech index. If you look at my first post - XBI has almost no correlation to the rest of the portfolio, but it has a very strong (0.8) correlation to VHT. This is why I dropped VHT from the portfolio.

I got to an equal weight biotech-tech-staples-utility-gold portfolio. Here it is compared to the previous portfolio without gold. Also, I subbed VHT and XBI to show the difference:

I didn't like how much on an influence XBI had on the portfolio as a whole:

So I trimmed the exposure from 20% to 15%. At this point there is an extra 5% that needs to be allocated to something on the low risk side of the portfolio - so gold-staples-utilities. I added Berkshire - but the 5% just needs to be invested somewhere less volatile and uncorrelated to tech or biotech.

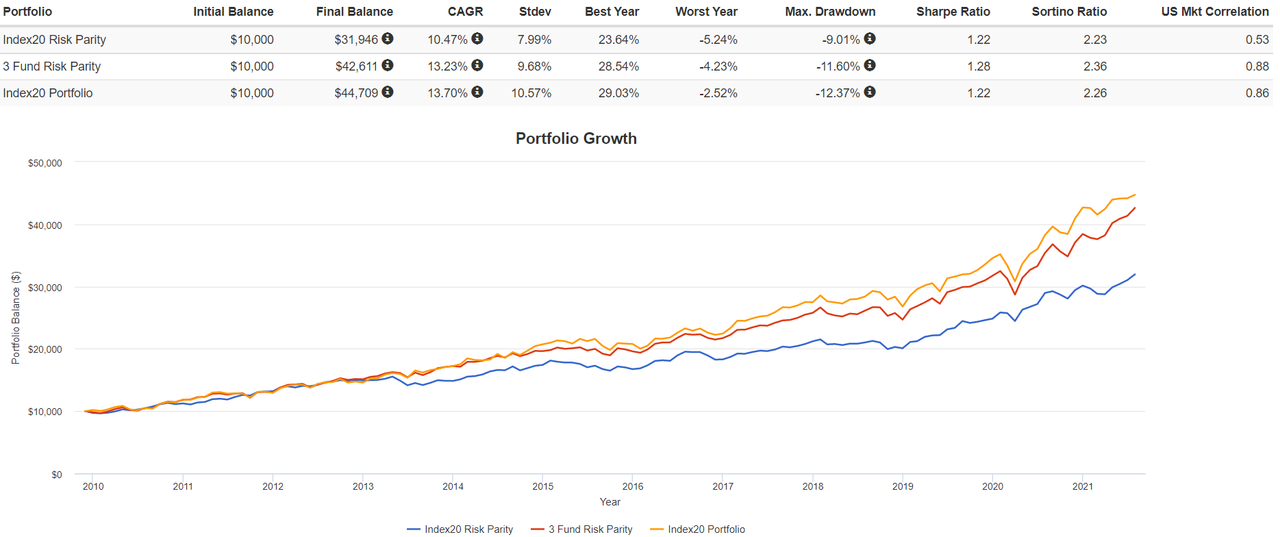

Bringing it full circle - here is how the proposed portfolio compares to the risk parity portfolios detailed in the thread referenced at the beginning of this post. The new portfolio is unleveraged (versus 40% leverage in the 3 fund risk parity and 20% in the index20 risk parity portfolio) and uses no bonds: