Even when there were the stock market crashes I never sold. While I do plan to retire in the next 10-12 years, the majority of my money will still be in the stock market for the long term since I will only be pulling out my yearly expenses when I retire. And my retirement period will be over a long time span > 30 years.

This from a 57-year-old who experienced the '87 crash, the dot-bomb and the great recession...

I would worry you underestimate the variability in possible outcomes for your plan and therefore wonder if maybe you need to reassess your capacity to bear risk. Especially if you've mostly been saving and accumulating since the Great Recession.

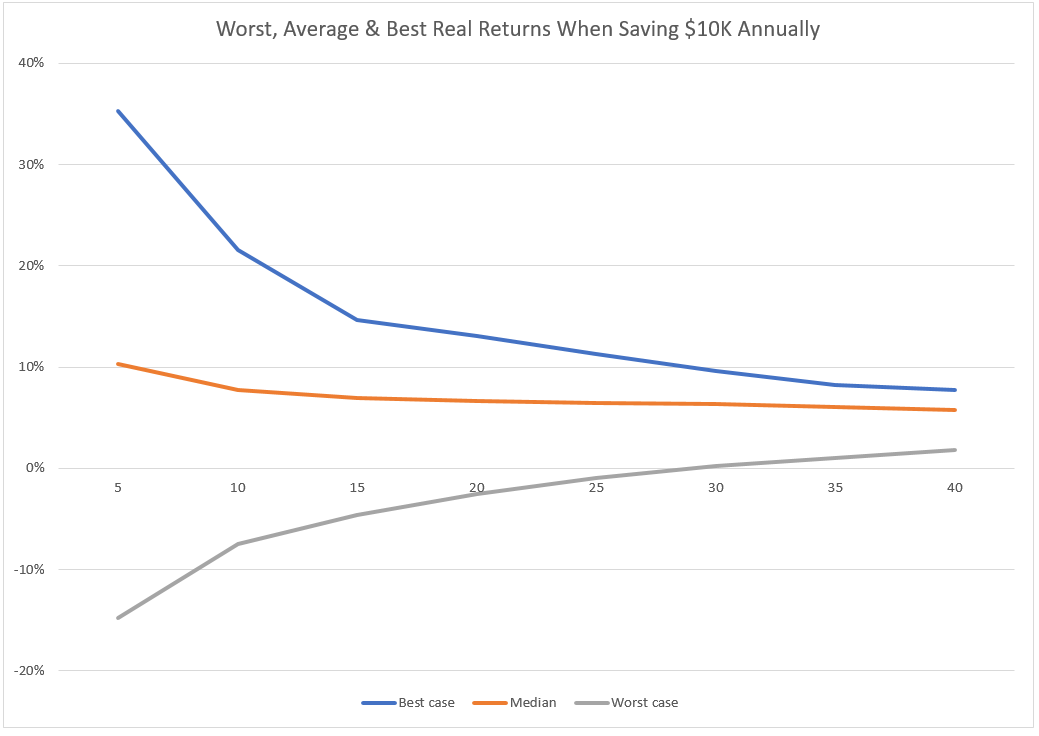

BTW, that isn't a gut feel or intuitive assessment. Your rather tight range of years of work left (10-12 years) suggests this. And yet for a ten-year horizon, the range of annual real returns runs from roughly -5% to 20%. The simple chart below shows this...

P.S. I used cfiresim and Excel and the data you provided to estimate your current wealth and savings rate ... It looks to me as if have $400K right now and are saving $15K a year. On average, that puts you to $1M in ten years using a 100% stocks allocation. But at the ten year marker, you might have only $350K... or you could have close to $3M...