I posted this at Bogleheads but am curious what the collective Mustache wisdom is:

I have decided to take a more proactive role in managing our money and found my way over here. I think that I have always been a pseudo Mustachian but not quite as refined or informed. I am trying to change that quickly but it seems there are endless topics! Currently I am studying asset allocation and tax implications in addition to taking Finance and Personal Finance on Coursera. Following that, I will be looking at implementing a college fund. All suggestions, criticisms, advice, etc. are greatly appreciated.

Here are my vitals:

Emergency funds: Six Months

Debt: $30,000 HEL, 5 year fixed at 2.0%

Tax Rate: 25% Federal, 4.35% State

State of Residence: Michigan

Age: 38

Yearly spending: $25,000

Desired Asset allocation: Currently researching

Desired International allocation: Currently researching

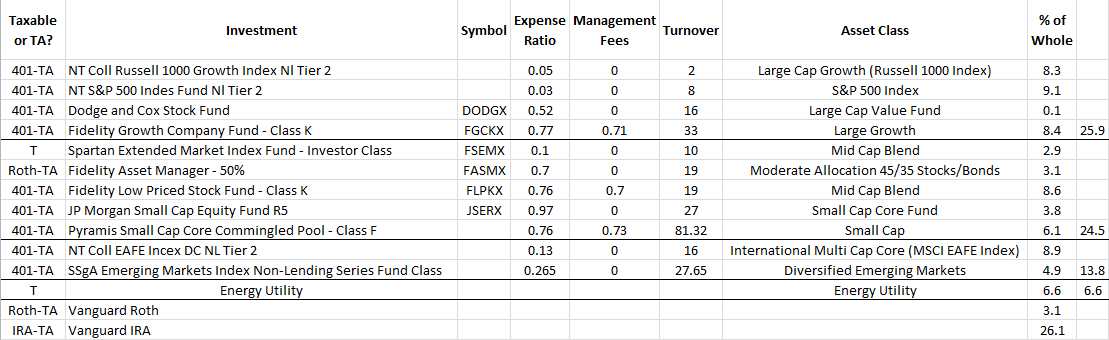

Current total portfolio, both taxable and tax advantaged is in the mid six figures:

Anticipated Annual Contributions:

$30,000 Taxable

$15,000 401k (Sum of employee and employer contributions)

$10,000 Roth

$10,000 College fund (as yet unidentified)

Additional info:

I am in the process of rolling a former employers 401k and a Fidelity Roth to Vanguard. I have reduced my current 401k contribution to maximize my employers match, but nothing additional. I would like to contribute more to a taxable account so that in 5-10 years I can increase my family time and supplement my income using investments. Also, the high ER 401k options above are likely to be converted to a Vanguard IRA as my wife's employment situation changes. The lower cost options are mine and so far I am happy with them.

So, on to the questions:

1. Any suggestions for an asset allocation? Based on the above details, I am not risk averse, should I be more conservative?

2. How would you allocate the 26% in the Vanguard IRA?

3. Should I DCA the Vanguard IRA rollover? It is currently set up to go into the Prime Money Market, the transfer should occur in the next 2 weeks or so.

4. How would you allocate the 3% in the Roth IRA?

5. Currently I have no exposure to Bonds, is that OK for now or should I be seeking a bond fund, in the taxable or tax-advantaged account?

6. College fund suggestions?

7. Are the annual contributions appropriate?

8. Am I completely off my rocker?

I look forward to the replies, suggestions, and subsequent research (this really is fun stuff)!

Thanks,

Wooderson