The flip side of this question, and what I thought this thread was going to be about, is how many years of retirement you're currently giving away by not reducing your spending.

For most people, it works out to about one extra years of retirement for every 1% reduction in your current pay that you devote to savings instead of spending (it's more than one year for the first few percent, less than one year for the later percentages). So for example, increasing your savings rate from 20% to 30% (a 10% increase) moves your retirement age up from age 60 to age 50 (10 extra years of retirement).

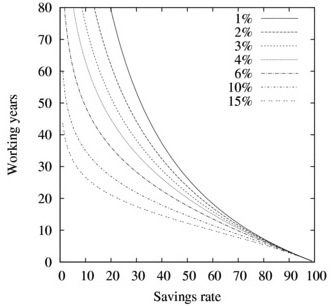

By this accounting, anyone who is still working is currently answering the question in the title of this thread with "I'm currently taking 1% of my salary to lengthen my working career by one year". You could instead buy one additional year of retirement by saving an extra 1%. For your exact number, spend some time understanding the following graph. The slope of each line, at each savings rate, is how many years you of retirement buy with each additional percent of savings. It's much more than one year if you currently save 5%. It's only about three months more per each additional percent saved if you're already saving 60%.

Poll

Poll