Life SituationMyself and my wife (both in late 30s), with two kids under 5. We live in a small house (1000 sq ft), which is fairly old (1946), and poorly constructed, in the urban center of a fast-growing, non-coastal city in the U.S. I work pretty long hours, travel quite a bit for work, and have had relatively little time for extracurricular pursuits / outside interests over the past ~6 years. Wife spends lots of high quality (albeit exhausting) time raising our children (as we planned and hoped for), while juggling two part-time freelance jobs.

Gross Salary/WagesI am full-time employed in information security; wife works two part-time freelance gigs. I own a single member LLC; side projects for which add modest income and periodic stress. Between base salary, typical bonus, and occasional side projects, my gross income averages about $160k; wifes supplemental income ~$12k. Total gross income: $172k.

Pre-tax Deductions4% 401k deduction with (max) 4% company match. Company-subsidized family medical insurance - relatively low deductible plan (only because its heavily subsidized). Long-term disability insurance for me, and vision plan for wife & I. No dental insurance (until kids get older at least).

Net IncomeApprox. take home after subtracting taxes, SS, and other deductions (but including 401k):

$120-125kInterest & Dividends~$3.5k /yr (mostly dividends at this point as were pretty heavily weighted towards dividend-favorable investments, and APY for bank accounts is so miserably low)

Business ExpensesApprox $5k/yr (professional insurance, computing equipment / hosting services, meals out, sporadic travel expenses for my SMLLC, and wifes freelance work)

TaxesNo state income tax. (Partially as a result) property taxes are relatively high: ~$6k/yr (we contest the increase in valuation each year, with mixed success). Effective federal income tax rate of ~15%.

ExpendituresFirst off, a few important notes:

- Ive excluded house renovation costs - we generally consider these investments.

- Not necessarily investments in the financial sense - for various reasons most renovations in our property are not likely to return close to their full cost - but investments in our familys use of the property.

- Also excluding a possible new (used) car purchase as a one-time cost (which we will pay in cash).

- Conversely, Ive included company contributions towards medical insurance as expenditures, because we want to keep the true total cost ($1500/mo!) front of mind.

- We set an annual budget, and categorize all expenditures on a monthly basis to compare against budget.

We have no mortgage or car payments, and drive (a fuel efficient) car infrequently (4-5k miles/yr). Were fortunate enough to be a very healthy family to this point, and hold high quality, low deductible medical insurance. We use HVAC sparingly, generally prefer to eat home-cooked meals (including leftovers for lunch at work), and drink moderate amounts of alcohol.

The amount of money we spend, given the lack of debt payments and our frugalities, is a bit shocking. In 2015, we spent $66.5k (excluding renovation costs and (modest) side business expenses). Our budget this year is $83k note, however that the entire difference is due to incorporating true medical insurance costs this year, for the first time. (In other words, we are not actually spending $83k (thanks to company subsidies - our actual out-of-pocket total is about $70k), but would if self-employed / retired and retained this insurance plan)

We are currently at 87% of budget year to date (i.e., operating at 13% under per month) so, on target for

$72k of expenditure equivalent in 2016 (again, including full medical insurance cost, but excluding renovations and possible vehicle purchase).

Our most significant expenditure categories are:

- Medical insurance ($1500/month) (again, including company subsidy as an expense)

- Groceries ($1450/month)

- Property taxes ($6000/year)

- Child care ($450/month) (part-time pre-school and babysitters)

- Dining ($400/month)

- Travel ($3000/year) (several visits to out of state family, or to support their visits to us)

Despite the higher-than-expected figure, I dont think we need a great deal of advice around trimming expenditures - we already know where wed begin cutbacks if our income were to decline significantly:

- Housing: $100/mo reduction (Cleaning and fixing as many issues as possible ourselves; being even more frugal with climate control)

- Groceries and dining: $300/mo reduction (A common source of discussion and one of the few points of disagreement between my wife and I (she places high value on quality, healthy, and interesting food; I view food primarily as sustenance))

- Child care: $300/mo reduction

- Medical insurance: $500/mo reduction (Seems very possible wed be able to even further reduce these rates (based on http://www.mrmoneymustache.com/2011/09/21/i-can-never-retire-because-of-health-insurance-waaah-waaah/), but havent really dug into this yet - so, estimating savings somewhat conservatively here)

- Travel: $600/yr reduction

Wed be looking at annual expenditures of $15k less if we could achieve just these cutbacks - which would put our reduced annual expenditure rate at $57k. If retired, Id hope and expect we can find ways to make this even lower. Further down the road (~20 years), I expect our expenditures will decrease once the kids are out of the house / independent. Very rough estimate of $12k less (primarily between lowered / eliminated child care and food costs) = $45k/yr post-kid retirement expenditures. If we estimate 50 years of life remaining, with 20 years of $57k annual expenditures, and 30 years of $45k, we arrive at a nice round average of

$50k annual expenditures over 50 theoretical retirement years.

AssetsOur house is paid off (and has been since five years after purchase). It might sell right now for close to $400k, but the market is frothy - Id estimate $350k more reasonably.

Important tangent: We live in one of the hottest real estate markets in the country (for five years running) - but our house is old, small, and poorly constructed (have I mentioned that?). Due to heritage trees and other building restrictions in our neighborhood, a future owner could not simply tear down the house and build a much larger house. By our estimation, this caps our property value lower than many surrounding properties. We paid $205k for the property in 2009 - which at first blush makes it seem like quite the investment - but weve poured nearly $100k into renovations (no time available to do much ourselves) to make it more livable since then. Due to the structural deficiencies, regulatory limits on expansion, and other issues with the property (poor neighborhood schools, etc.), we shouldnt invest / spend much more in this property (strictly financially speaking, weve already invested too much).

Also: for all of my complaints about the poor construction of our house (and our loud neighborhood), we love living here. The small house suits our family just fine (at least for a few more years), and were in close proximity to many amenities - parks, libraries, restaurants / taco stands, swimming pools, running trails, office, etc. We mostly bike or walk as a result, and wed be very hesitant to give this up.

Our vehicle (2009 Honda Fit) is paid off. (We are on the verge of replacing this with a used Prius v, which will set us back approx. $10-12k after trade-in)

LiabilitiesNone, beyond monthly credit card balances (paid in full each month).

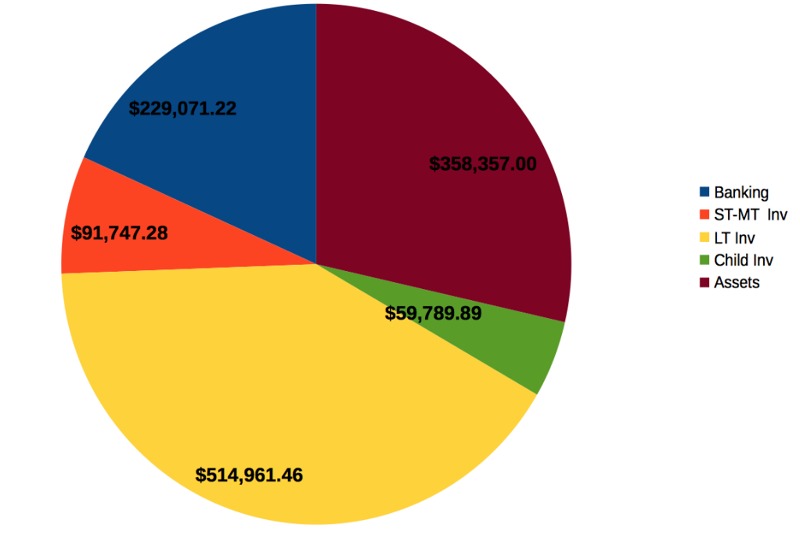

Current Asset Allocation

Notes:

- Long term investments: IRA, Roth IRA, SEP, 401k/403b

- Short-Medium term investments: other (non-retirement) investment holdings

- Childrens investments: 529 savings plan funds

- In accounts which we have full control over, we invest almost entirely in low cost, relatively broad market ETFs.

- Social Security funds are not included here (I guess because I dont consider it truly guaranteed to be there for us in 30-40 years). According to our latest statements, our estimated benefits at "full retirement age" (67!) are between $1,200-1,300 / month.

Financial Independence CalculationsGoing on the following assumptions and numbers documented in

http://www.mrmoneymustache.com/2012/01/13/the-shockingly-simple-math-behind-early-retirement/:

- earn 5% investment returns after inflation during saving years

- live off of the 4% safe withdrawal rate after retirement

- want the Stash to last forever, so only touching the gains

To apply it in real life, just take your annual spending level, and multiply it by 25. Thats how much you need to retire, at the most.At our current spending levels ($72k/yr), we'd need $1.8M of

income-producing funds to retire.

Our current total "net worth" is $1.22M - but this includes non-liquid / non-income producing assets such as our house/property, and child education funds. Excluding these categories leaves us with total current investable assets of $810,000. (Note: non-retirement account investable assets are only about $300k.

How important to the calculation is this distinction?).

Based on these figures, we would need another $1M of investable assets until FI. According to networthify, at our current savings rate (about $50k/yr), this would require a bit over 9 years (

https://networthify.com/calculator/earlyretirement?income=122000&initialBalance=810000&expenses=72000&annualPct=5&withdrawalRate=4).

(Side note: I generally find networthify.com a bit too simplistic / inflexible, but

www.firecalc.com is the polar opposite too complicated for me to have high confidence in the results, based on uncertainty of my inputs)

However:

- We can trim expenditures, as documented above particularly with more time available to DIY. As previously mentioned, weve estimated a more frugal lifestyle at approximately $57k/yr, which lowers our target figure to $1.425M. This would require about 5 years at our current income and savings rate (i.e., assuming no additional significant one-time costs for renovations, major medical expenditures (up to out of pocket insurance maximums) etc.) (https://networthify.com/calculator/earlyretirement?income=122000&initialBalance=810000&expenses=57000&annualPct=5&withdrawalRate=4). Taking into account lower expenditures once the kids are independent, our target figure would be closer to $1.25M, requiring about 4 years (although Im sure these calculations are not quite accurate, given that the lower expenditures only come into play down the road (https://networthify.com/calculator/earlyretirement?income=115000&initialBalance=810000&expenses=50000&annualPct=5&withdrawalRate=4)).

- As espoused by MMM (and common sense), neither wife nor I intend to fully retire any time soon. I would like to spend a portion of my time continuing to work on the difficult, interesting (and lucrative) problems of information security, and would love to learn some other useful skills that may lead to income eventually, or at least bartering with friends.

- I am likely more interested in a sabbatical than early retirement / financial independence at this point. Ive become almost completely burnt out on my work over the past 2-3 years, which is disheartening to say the least (I was extremely enthusiastic about my work for the first 10 years of my career).

Considerations / Questions / Dilemmas- 1) Regarding asset allocation / investment decisions: As per the pie chart above, the vast majority of our investment holdings are in (tax-advantaged) retirement accounts (IRA, Roth IRA, SEP, and 401k/403b). Ive long wondered if we might be contributing too much money to these accounts at this point.

- 1b) Based on http://www.mrmoneymustache.com/2011/11/11/how-much-is-too-much-in-your-401k/, it seems the answer is likely yes. More details: "Enough to live on for a good 30 years, from age 60 through 90." Rough estimate that wife and I could live on $30k per year in today's dollars. "Assume that you can safely withdraw about 5% per year from your fund from a combination of its investment returns/dividends and a bit of its principal" = we need $600k in todays dollars by 2038. "Assume investments can grow at 5% after inflation", by 2038 (age 60) our current ~$500k retirement fund should = $1.462M ((1.05 ^ 22) * 500k)

- 1c) Based on this calculation, we already have too much in our various retirement accounts, and now just need funds to get us from now until age 60.

- 1d) Fortunately it seems there's a reasonable way to take excess funds out of these retirement accounts down the road at least for the 401k (the Roth IRA Escape Hatch Loophole) (I havent closely read / fully grokked this yet)

- 1e) Am I correct in surmising that we should drastically shift our investments towards more liquid accounts? (i.e. those that we can withdraw from without penalties prior to age ~60) Or are the tax benefits of continued funding to 401k, IRA, Roth IRA, etc. worth the lack of available funds in the interim / the hassle of needing to exploit loopholes to access funds down the road? (also, are there similar loopholes for withdrawing funds early from traditional and Roth IRAs?)

- 2) Should we consider hiring a financial advisor? My frugal nature of course shouts no, but I can think of 3-4 financial snafus over the past several years that have cost us significant money (primarily not having funds available in our investment accounts at the right time to buy in when markets crash). On the other hand, these lapses are mainly attributable to my lack of time due to being too busy with work, a problem which would presumably go away in semi-retirement..) (Note: weve also looked into robo investing services, but found them unsuitable for various reasons - and, they would not serve our primary need of personalized financial advice / sanity checks.)

- 3) Ongoing concerns about a future economic instability: if the market crashes a few years after we reach FI, taking our balance from, say, $1M to $600k, presumably the job market would tank along with it. Trying to re-enter the job market with a multi-year gap on the resume and rusty technical skills is a harrowing prospect (especially as a 40-something in the high tech sector).

- 4) One of my biggest hangups to retiring, taking a sabbatical, or working part time is the opportunity cost: I am currently entering my peak earning years in an extremely hot and therefore lucrative field, with in-demand skills. Every month I choose not to work equates to approximately $13,000 of lost income ($10k after taxes). For a family focused on financial independence, thats very difficult to accept.

- 5) Separate but relatedly: Im in my late 30s, and work in high tech. Without spending significant amounts of time outside of $dayjob, I expect to (continue) slowly falling behind the curve on the latest and greatest technology. As such, my marketable job skills have a shelf life. (Although, if stories of modern day, high-paid mainframe programmers are to be believed, theres probably a very long tail to this)

- 6) Living in a medium-sized, quickly growing city, dominated by high tech and other high income jobs means competition for housing is fierce. Subjectively, it seems a significant portion of the population of this city is more money driven than ourselves. All of this means we feel pretty locked in to our current property, despite its shortcomings.

- 7) The aforementioned excluded expenditures (primarily house renovations) have significantly slowed the growth in our net worth / progress towards FI (again, since we consider the increase in property value to represent only a portion of the cost). This is frustrating and a bit demoralizing, but has been necessary to accommodate a growing family in our current location.

- 8) Once I leave full time employment, wed like to do some traveling as a family. While wife and I have always been fairly frugal travelers, traveling with two kids will change that dynamic somewhat (4 airfare tickets, for example!). This obviously would increase our expenditures.

- 9) Note regarding our childrens 529 savings plans: we will probably cut off contributions once both accounts reach approximately $40k. Wed like to steer our children towards some combination of community college or public schools, trade school, partially paying their way through college, or taking advantage of no cost / low cost online education as it continues to proliferate and mature.

- 10) My job involves identifying weaknesses and risks in IT systems. As evidenced by recent headlines, there are many. The financial industry, while better than most, is far from immune. Many people dont fully understand just how difficult it is to detect advanced intrusions, and effectively remediate these situations. I dont sleep very well at night knowing that 99% of our wealth is stored electronically with third parties, and we have only monthly electronic statements to show for it. Catastrophic failures in the US and worldwide financial systems as a result of hacking (particularly nation state-sponsored activities) are not outside the realm of possibility. While I try not to live in a world of dire pessimism, and I understand some Mustachians scoff at the idea of hoarding precious metals, is converting a portion of our wealth (say 5%) to some form of cash / precious metal / bitcoin really a foolish idea? I understand these assets are not likely to increase in value over time the way that stocks have historically (in fact most physical assets are likely to depreciate due to inflation), but in the event of calamity affecting our infrastructure a few thousand dollars worth of cash and metals would probably be more useful than PDF copies of investment statements, right?

Plan Going ForwardMore realistic (and more desirable) than continuing to work long hours with a goal of retiring in 5-9 years is working moderate / varying amounts over the next 10-20 years.

As such, a big question right now is,

How much income do we need in order to not cut into our investment holdings? (i.e., just live off of income and whatever interest we can currently reap)

- At current spending levels: $32k/year ($800k investments * 5% interest (after inflation) = $40k; remainder must come from income)

- At frugal expenditure level: $17k/year

Conclusion: As long as we generate $17-32k of income each year, we do not need to be concerned with draining our retirement savings, which are already (more than) sufficiently funded for retirement at age 65. Any income beyond these thresholds would bring us closer to reaching complete financial independence prior to age 65.