Sure, that is obvious. But I think OP is thinking they might go just over the threshold, rather than $40,000 over it. Which means they make $5k in extra income and maybe lose $5k in tax credits, effectively wasting their time.

An increase in W-2 (or self-employment) earnings won't cause that with the Earned Income Credit (EIC). What can make the EIC go away with $1 more is interest/dividends/capital gains/rental income: any investment income >$3500 means no EIC.

Another "step change" (aka "tier") occurs with the saver's credit.

Looks like going from 51k to 60k in one of the above scenarios causes a 22% effective tax rate, plus state tax and FICA. So it would be up to OP whether the additional work is worth the effort.

The phase-out rate of the EIC with two children is a little over 21%. That applies when the greater of AGI or (W-2 plus self-employment) is between $24,350 and $51,492. Add that to the nominal tax bracket, and any other phase-outs, tiers, etc. to get the marginal rate.

Speaking of marginal rates, the

interpretation of the new CTC will have a large impact on the OP's situation.

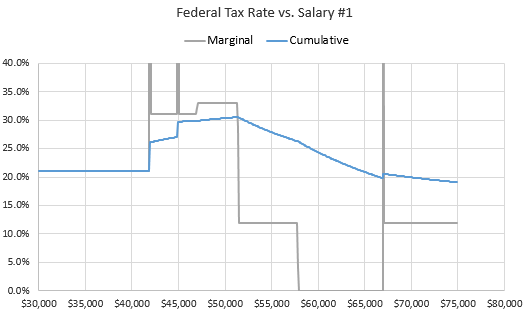

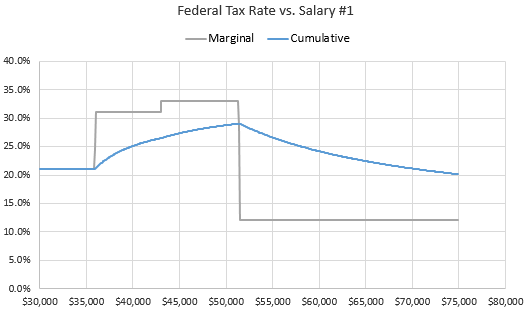

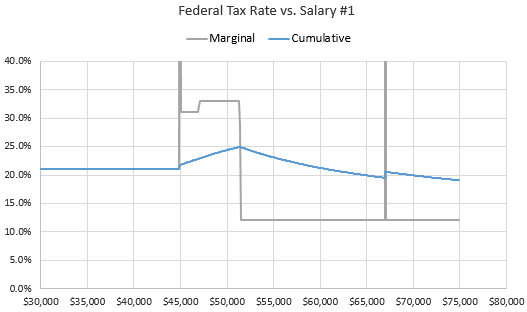

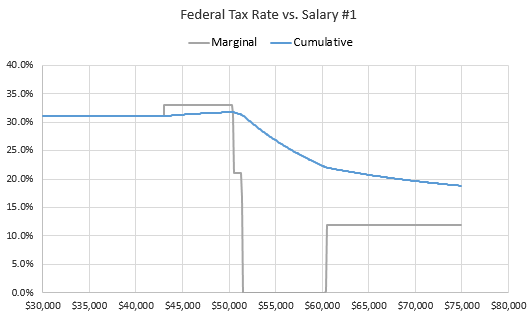

The charts below show marginal rates for W-2 income above $30K assuming

1) Optimistic CTC interpretation, no IRA contribution:

2) Optimistic CTC interpretation, $2K IRA contribution from each spouse:

3) Pessimistic CTC interpretation, no IRA contribution

4) Pessimistic CTC interpretation, $2K IRA contribution from each spouse: