This is a really brilliant* article. It reminds me of the pseudo-arguments used to sell variable annuities. It seems so... scientific and data driven, that the conclusions must be correct!

First, the author is very clever. He's indeed cherry picked 'facts' to try and attack index funds and (hopefully) convince people of the usual story from such financial advisor/investment funds:

1/ The stock market is a very risky place - look at this!

2/ At some time you will probably lose most of your money overnight! Remember 2008? 1999? 1931?

3/ If you invest in index funds you are only ever going to get at best average returns. So you're risking all your money for mediocre rewards, while having to invest in crazy overvalued companies like Facebook and Tesla.

4/ So give me your money, and for an insignificant fee I'll be very clever, and we'll work to preserve your capital and get great returns**.

5/ You probably haven't heard of a universal whole life variable annuity have you? You can never lose money! When the stock market goes down we insure you against any losses! And when the stock market goes up, you'll get a great return, tax free! Just sign here.

[*brilliantly evil and deceptive, that is]

[** past performance is not a guarantee of future returns.]

The whole article is filled with a lovely mix of pure bullshit, misleading analysis, 'bait & switch' tactics, cherry picked time periods and mutually inconsistent motherhood statements/non sequiters. It makes me want to scream at him the whole time.

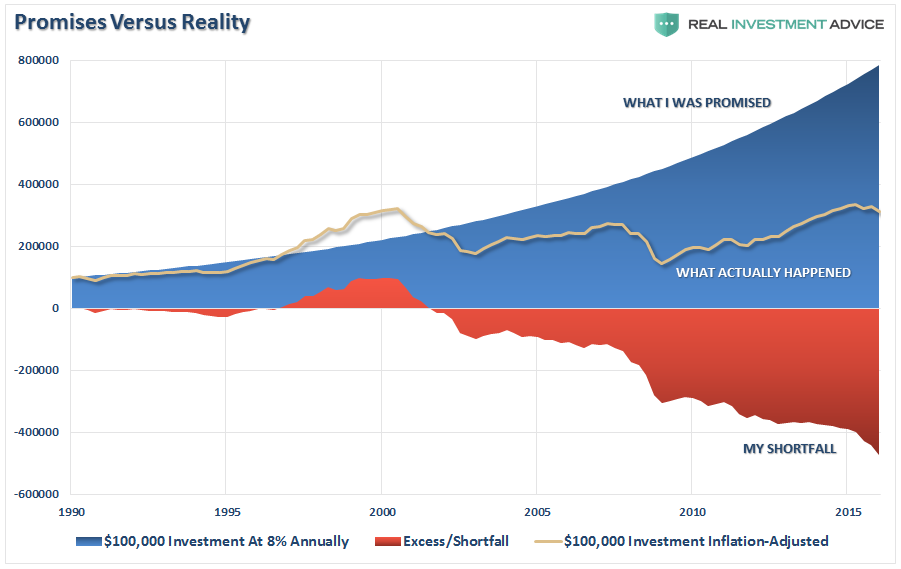

For example: He shows the SP500 index from 1990-2017 and claims it shows a terrible return.

The chart below shows the impact of losses on a portfolio as compared to the commonly perceived myth that investors average 8% annually in the stock market.

.

.

He thus compares a theoretical 8% CAGR (apparently a commonly perceived myth) against an

inflation corrected SP500 index number with no reinvestment of dividends, from 1990-2017. Wow, that's so apples to oranges, but it does have the 'advantage' of making the "index" seem to lose $500k! Why is this so evil?

1/ He claims 8% is 'promised'. OK, but typically this 'promise' is nominal and includes both inflation and dividends.

2/ He then compares this against a bare index that he deflates to make it 'real', and

3/ Does not reinvest dividends

4/ Makes the analysis very time period dependant because he never makes any periodic contributions.

Eyeballing his chart he claims the initial $100k in the SP500 ended up 27 years later at ~$300k (real), leaving a supposed 'shortfall' of $500k.

However, when I use

https://www.portfoliovisualizer.com/ I get very, very different results from ol' Lance (he's a Chief Portfolio Strategist/Economist you know).

In actuality, such an investment of 100% US stocks for $100,000 in 1990 grew by 2017 to a nominal $1,330,000, or $685,000 in 1990 dollars after inflation correction. That's a

real CAGR of about 7.7% (In fact, from 1990-2017 with 100% US market we get a nominal CAGR of 9.7%, easily beating his strawman! LOL.)

In another example he uses a hypothetical 35 year old, but this idiotic 35 yr old neither makes any further regular contributions after the initial investment, nor does he compound his dividends post investment, and he seems to always invest in periods with some big drops in the index. Little wonder his 'returns' totally suck (according to Lance that is).

He also fills the article with the sort of meaningless down-home fortune cookie homilies that'll have grandad nodding like a bobblehead, such as "You can replace lost capital but you cant replace lost time" and the improtance of "Capital preservation", plus pseudo-fact sounding claptrap like "The impact of losses, in any given year, destroys the annualized compounding effect of money."

The article makes me angry. I just hate the idea of older people reading this type of total bullshit and thus being convinced to let this idiot manage their money. I'd bet dollars to donuts he'll be selling them some kind of zero liquidity variable annuity / whole life shit or analgous products. So they're 'protected' and sure to 'meet their goals'.

Grrrrr.